“Securing Tomorrow: Balancing Growth and Stability in Your Golden Years.”

Introduction

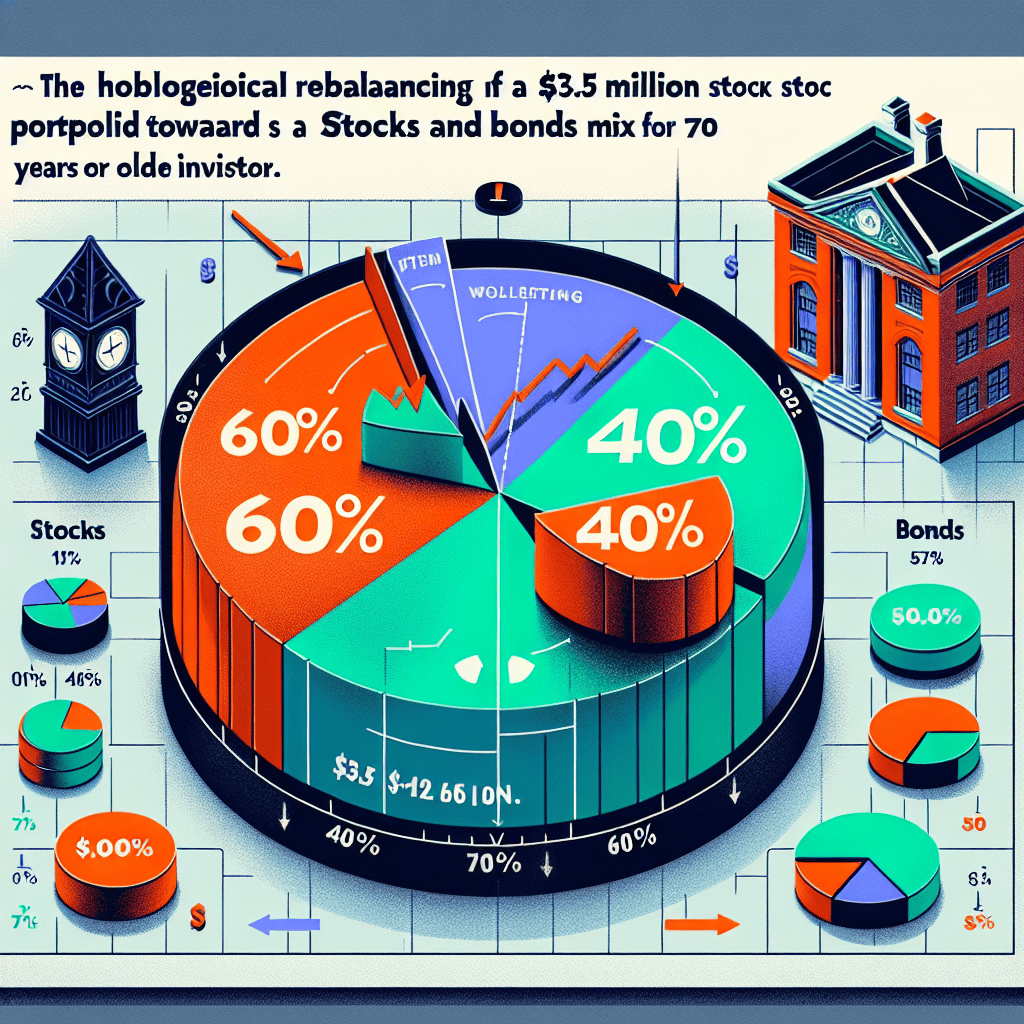

As individuals approach or enter their retirement years, the question of how to manage and preserve accumulated wealth becomes increasingly critical. For those with a substantial stock portfolio, such as one valued at $3.5 million, the decision to rebalance to a more conservative asset allocation, like a 60/40 mix of stocks and bonds, is a common consideration. This strategy aims to reduce risk and provide more stable income during retirement. However, the decision is not straightforward and involves evaluating various factors, including life expectancy, income needs, market conditions, and personal risk tolerance. Understanding the potential benefits and drawbacks of rebalancing to a 60/40 portfolio at age 70 or older is essential for making an informed decision that aligns with long-term financial goals and retirement plans.

Understanding the 60/40 Portfolio Mix: Is It Right for Retirees?

As individuals approach retirement, the question of how to best manage their investment portfolios becomes increasingly pertinent. For those with a substantial portfolio, such as $3.5 million, the decision to rebalance to a 60/40 mix of stocks and bonds is a common consideration. This traditional allocation strategy, which consists of 60% equities and 40% fixed-income securities, has long been favored for its balance of growth potential and risk mitigation. However, the suitability of this approach for retirees, particularly those over the age of 70, warrants careful examination.

To begin with, the 60/40 portfolio mix is designed to provide a moderate level of risk while still offering the potential for growth. Equities, which make up 60% of the portfolio, are included for their ability to generate higher returns over the long term. Meanwhile, the 40% allocation to bonds serves to reduce volatility and provide a steady income stream. This combination has historically been effective in smoothing out the fluctuations of the stock market, making it an attractive option for those seeking a balanced approach.

Nevertheless, as investors age, their risk tolerance often decreases, prompting a reevaluation of their asset allocation. For retirees in their 70s, the primary concern typically shifts from accumulation to preservation of capital and income generation. In this context, the 60/40 mix may still be appropriate, but it is crucial to consider individual circumstances, such as life expectancy, health status, and financial goals. For instance, those with a longer life expectancy may still benefit from a higher equity exposure to combat inflation and ensure their portfolio lasts throughout retirement.

Moreover, the current economic environment plays a significant role in determining the appropriateness of the 60/40 mix. In recent years, low interest rates have diminished the income-generating potential of bonds, leading some experts to question the efficacy of this traditional allocation. As a result, retirees may need to explore alternative fixed-income investments or adjust their equity exposure to achieve their desired income levels. Additionally, the potential for rising inflation could erode the purchasing power of fixed-income returns, further complicating the decision-making process.

Another factor to consider is the tax implications of rebalancing a portfolio. Selling assets to achieve a 60/40 mix may trigger capital gains taxes, which could significantly impact the overall value of the portfolio. Retirees should consult with a financial advisor or tax professional to assess the potential tax consequences and explore strategies to minimize their tax burden.

Furthermore, it is essential to recognize that the 60/40 mix is not a one-size-fits-all solution. Each retiree’s financial situation is unique, and a personalized approach is necessary to ensure that their portfolio aligns with their specific needs and objectives. This may involve adjusting the allocation to better reflect their risk tolerance, income requirements, and legacy goals.

In conclusion, while the 60/40 portfolio mix has been a longstanding strategy for balancing growth and risk, its suitability for retirees over 70 depends on a variety of factors. By carefully considering individual circumstances, economic conditions, and tax implications, retirees can make informed decisions about whether to adopt this allocation or explore alternative strategies. Ultimately, the goal is to create a portfolio that provides financial security and peace of mind throughout retirement.

Evaluating Risk Tolerance at 70+: Should You Rebalance Your Portfolio?

As individuals enter their 70s, the question of whether to rebalance a $3.5 million stock portfolio to a 60/40 mix becomes increasingly pertinent. This decision hinges on several factors, including risk tolerance, financial goals, and life expectancy. At this stage in life, the primary concern often shifts from wealth accumulation to wealth preservation and income generation. Therefore, evaluating one’s risk tolerance is crucial in determining the appropriate asset allocation.

Traditionally, the 60/40 portfolio mix, consisting of 60% equities and 40% fixed-income securities, has been considered a balanced approach. It aims to provide growth potential through stocks while offering stability and income through bonds. However, the suitability of this mix for someone over 70 depends on individual circumstances. For instance, if an investor has a high risk tolerance and a longer life expectancy, they might prefer to maintain a higher equity exposure to capitalize on potential market gains. Conversely, those with a lower risk tolerance or shorter life expectancy might lean towards a more conservative allocation to safeguard their assets.

Moreover, the current economic environment plays a significant role in this decision. With interest rates fluctuating and market volatility ever-present, the traditional 60/40 mix may not always deliver the expected results. In recent years, low bond yields have prompted some investors to seek alternative income-generating assets, such as dividend-paying stocks or real estate investment trusts (REITs). These alternatives can offer higher returns but also come with their own set of risks. Therefore, it is essential to assess whether these options align with one’s risk tolerance and financial objectives.

Another factor to consider is the potential impact of inflation on a retiree’s purchasing power. As inflation erodes the value of money over time, maintaining a portion of the portfolio in equities can help counteract this effect, given their historical tendency to outpace inflation. However, this strategy requires a careful balance, as excessive exposure to stocks can increase the portfolio’s volatility, which may not be suitable for all retirees.

Furthermore, tax implications should not be overlooked when contemplating a portfolio rebalance. Selling appreciated assets to achieve a desired allocation can trigger capital gains taxes, which could significantly impact the portfolio’s overall value. Therefore, it is advisable to consult with a financial advisor or tax professional to explore tax-efficient strategies, such as tax-loss harvesting or utilizing tax-advantaged accounts, to minimize the tax burden.

In addition to financial considerations, personal factors such as health status, lifestyle preferences, and legacy goals should also influence the decision to rebalance. For instance, those with significant healthcare expenses may prioritize liquidity and stability, while others may wish to leave a substantial inheritance and thus opt for a more growth-oriented approach.

Ultimately, the decision to rebalance a $3.5 million stock portfolio to a 60/40 mix at 70+ is not a one-size-fits-all proposition. It requires a comprehensive evaluation of one’s risk tolerance, financial goals, and personal circumstances. By carefully considering these factors and seeking professional guidance, retirees can make informed decisions that align with their long-term objectives and provide peace of mind in their golden years.

The Impact of Market Volatility on a $3.5 Million Portfolio

As investors age, the question of whether to rebalance a stock portfolio to a more conservative allocation becomes increasingly pertinent. For those with a $3.5 million portfolio, the decision to shift to a 60/40 mix of stocks and bonds, particularly for individuals over 70, is influenced by several factors, including market volatility, risk tolerance, and financial goals. Understanding the impact of market volatility on such a substantial portfolio is crucial in making an informed decision.

Market volatility can significantly affect the value of a stock-heavy portfolio. While stocks have historically provided higher returns over the long term, they are also subject to short-term fluctuations that can be unsettling, especially for retirees who may rely on their investments for income. A 60/40 mix, which typically involves 60% in stocks and 40% in bonds, is often recommended for those seeking a balance between growth and stability. This allocation aims to reduce exposure to market swings while still allowing for some capital appreciation.

The primary advantage of rebalancing to a 60/40 mix is the potential for reduced volatility. Bonds, generally considered safer than stocks, can provide a buffer during market downturns. This stability can be particularly appealing for investors over 70, who may prioritize preserving capital over aggressive growth. Moreover, a diversified portfolio can help mitigate the impact of market volatility, as different asset classes often react differently to economic events.

However, it is essential to consider the potential trade-offs. While a 60/40 mix may offer more stability, it could also result in lower overall returns compared to a stock-heavy portfolio. For some investors, the opportunity cost of reduced growth potential may outweigh the benefits of decreased volatility. Additionally, with increasing life expectancies, retirees may need their portfolios to last longer, necessitating a careful balance between risk and return.

Another factor to consider is the current economic environment. Interest rates, inflation, and market conditions can all influence the performance of stocks and bonds. In periods of low interest rates, for example, bond yields may be less attractive, potentially diminishing the benefits of a 60/40 allocation. Conversely, in times of high inflation, stocks may offer better protection against the erosion of purchasing power.

Furthermore, individual circumstances play a crucial role in determining the appropriate asset allocation. Factors such as other sources of income, health care needs, and estate planning goals should be taken into account. For some, maintaining a higher stock allocation may be feasible if they have sufficient income from other sources or a strong desire to leave a financial legacy.

Ultimately, the decision to rebalance a $3.5 million portfolio to a 60/40 mix at 70+ should be guided by a comprehensive assessment of personal financial goals, risk tolerance, and market conditions. Consulting with a financial advisor can provide valuable insights and help tailor a strategy that aligns with individual needs and preferences. By carefully weighing the potential benefits and drawbacks, investors can make informed choices that support their long-term financial well-being amidst the challenges of market volatility.

Diversification Strategies for High-Net-Worth Individuals Over 70

As individuals age, particularly those who have accumulated significant wealth, the question of how to manage and preserve that wealth becomes increasingly pertinent. For high-net-worth individuals over the age of 70, the decision to rebalance a $3.5 million stock portfolio to a 60/40 mix of stocks and bonds is a topic worthy of careful consideration. This decision is not merely about numbers; it involves a nuanced understanding of risk tolerance, life expectancy, and financial goals.

Traditionally, the 60/40 portfolio mix has been a staple in investment strategies, offering a balance between growth and income. The rationale behind this allocation is to provide a cushion against market volatility while still allowing for capital appreciation. For those in their 70s, this strategy can be particularly appealing as it aims to reduce exposure to the inherent risks of the stock market, which can be especially volatile. However, it is essential to recognize that the appropriateness of this strategy depends on individual circumstances.

One of the primary considerations for rebalancing to a 60/40 mix is risk tolerance. As individuals age, their ability to recover from significant market downturns diminishes. A more conservative allocation can help mitigate this risk, providing a more stable income stream through bonds, which are generally less volatile than stocks. However, it is crucial to assess whether this reduced risk aligns with the individual’s financial goals and lifestyle needs. For some, maintaining a higher equity exposure might be necessary to achieve desired returns, especially if they have a longer life expectancy or wish to leave a substantial legacy.

Moreover, life expectancy plays a critical role in determining the appropriate asset allocation. With advancements in healthcare, many individuals are living longer, which may necessitate a more aggressive investment strategy to ensure that their portfolio lasts throughout their lifetime. In such cases, a 60/40 mix might be too conservative, potentially leading to insufficient growth to outpace inflation and meet long-term financial needs. Therefore, it is vital to consider personal health, family history, and lifestyle when deciding on the right balance.

Additionally, the current economic environment should not be overlooked. Interest rates, inflation, and market conditions can significantly impact the performance of both stocks and bonds. In periods of low interest rates, for instance, the income generated from bonds may be insufficient, prompting a reevaluation of the fixed-income portion of the portfolio. Conversely, in a high-inflation environment, equities might offer better protection against the eroding purchasing power of money. Thus, staying informed about economic trends and adjusting the portfolio accordingly is essential.

Furthermore, tax implications are another factor to consider. Rebalancing a portfolio can trigger capital gains taxes, which can be substantial depending on the size of the portfolio and the gains realized. High-net-worth individuals should consult with financial advisors to explore tax-efficient strategies, such as tax-loss harvesting or utilizing tax-advantaged accounts, to minimize the tax burden associated with rebalancing.

In conclusion, while a 60/40 portfolio mix may offer a balanced approach for some high-net-worth individuals over 70, it is not a one-size-fits-all solution. Each individual’s unique circumstances, including risk tolerance, life expectancy, economic conditions, and tax considerations, must be carefully evaluated. Engaging with financial professionals to tailor a strategy that aligns with personal goals and needs is crucial in making informed decisions about portfolio diversification and asset allocation.

Pros and Cons of Rebalancing to a 60/40 Mix in Retirement

As individuals approach retirement, the question of how to manage their investment portfolio becomes increasingly pertinent. For those with a substantial portfolio, such as $3.5 million, the decision to rebalance to a 60/40 mix of stocks and bonds is a common consideration. This strategy, traditionally seen as a balanced approach, aims to provide both growth and stability. However, the decision to rebalance at the age of 70 or older involves weighing several pros and cons.

On the one hand, rebalancing to a 60/40 mix can offer a sense of security. As retirees age, the need for a steady income stream becomes more critical, and bonds are generally perceived as less volatile than stocks. By increasing the bond allocation, retirees may reduce the risk of significant losses during market downturns, thereby preserving capital. This stability can be particularly reassuring for those who rely on their portfolio for living expenses, as it helps ensure that funds are available when needed.

Moreover, a 60/40 mix can still provide growth potential. While bonds offer stability, maintaining a 60% allocation in stocks allows for continued participation in market gains. This balance can help protect against inflation, which is a crucial consideration for retirees who may face rising costs over the years. By keeping a portion of the portfolio in equities, retirees can potentially achieve returns that outpace inflation, thereby preserving their purchasing power.

However, there are also drawbacks to consider. One potential downside of rebalancing to a 60/40 mix is the opportunity cost associated with reducing stock exposure. Historically, stocks have outperformed bonds over the long term, and by shifting a significant portion of the portfolio into bonds, retirees may miss out on higher returns. This could be particularly concerning for those who have a longer life expectancy and need their portfolio to last for several decades.

Additionally, the current economic environment plays a crucial role in this decision. Interest rates, for instance, are a significant factor in bond performance. In a low-interest-rate environment, bonds may offer limited returns, which could diminish the overall effectiveness of a 60/40 strategy. Retirees must consider whether the potential stability offered by bonds is worth the trade-off in terms of lower returns.

Furthermore, personal circumstances and risk tolerance should guide the decision-making process. Some retirees may have other sources of income, such as pensions or Social Security, which could allow for a more aggressive investment strategy. Others may have a lower risk tolerance and prefer the peace of mind that comes with a more conservative allocation. It is essential to assess one’s financial situation, goals, and comfort with market fluctuations before making any changes to the portfolio.

In conclusion, rebalancing a $3.5 million stock portfolio to a 60/40 mix at the age of 70 or older involves careful consideration of both the benefits and drawbacks. While this strategy can offer stability and some growth potential, it also comes with the risk of lower returns and the impact of current economic conditions. Ultimately, the decision should be based on individual circumstances, risk tolerance, and long-term financial goals. Consulting with a financial advisor can provide valuable insights and help retirees make informed choices that align with their unique needs and aspirations.

Financial Planning for Seniors: Maintaining Growth and Stability

As individuals enter their golden years, financial planning takes on a new dimension, focusing on maintaining a balance between growth and stability. For those with a substantial stock portfolio, such as a $3.5 million investment, the question of whether to rebalance to a 60/40 mix becomes particularly pertinent. This decision is crucial for seniors who aim to preserve their wealth while still seeking modest growth to outpace inflation and cover potential healthcare costs.

Traditionally, the 60/40 portfolio mix—comprising 60% equities and 40% fixed-income securities—has been a popular strategy for balancing risk and reward. Equities offer the potential for higher returns, which can be essential for maintaining purchasing power over time. Conversely, fixed-income securities, such as bonds, provide stability and income, which can be particularly appealing for those in retirement who may prioritize capital preservation.

However, the decision to rebalance a portfolio to this mix at the age of 70 or older requires careful consideration of several factors. First and foremost, one must assess their risk tolerance. As individuals age, their ability to recover from market downturns diminishes, making it crucial to evaluate how much risk they are comfortable taking. A 60/40 mix may still involve significant exposure to market volatility, which could be unsettling for some seniors.

Moreover, life expectancy plays a critical role in this decision. With advancements in healthcare, many individuals are living longer, necessitating a financial strategy that ensures their assets last throughout their lifetime. A portfolio heavily weighted in equities might offer the growth needed to support a longer retirement, but it also introduces the risk of significant losses during market downturns. Therefore, it is essential to strike a balance that aligns with one’s financial goals and expected lifespan.

Another consideration is the current economic environment. Interest rates, inflation, and market conditions can all influence the effectiveness of a 60/40 portfolio. In periods of low interest rates, the income generated from bonds may be insufficient to meet living expenses, prompting a reevaluation of the fixed-income allocation. Conversely, in a high-inflation environment, equities may be necessary to preserve purchasing power, but they also come with increased risk.

Tax implications are also a vital aspect of rebalancing a portfolio. Selling assets to achieve a desired allocation can trigger capital gains taxes, which could significantly impact the overall value of the portfolio. It is advisable to consult with a financial advisor or tax professional to explore strategies that minimize tax liabilities while achieving the desired asset allocation.

Furthermore, personal circumstances, such as health status and estate planning goals, should be factored into the decision-making process. For instance, those with significant healthcare needs may prioritize liquidity and stability over growth, while others may wish to leave a financial legacy for their heirs, influencing their risk tolerance and investment strategy.

In conclusion, rebalancing a $3.5 million stock portfolio to a 60/40 mix at the age of 70 or older is not a one-size-fits-all decision. It requires a comprehensive evaluation of individual risk tolerance, life expectancy, economic conditions, tax implications, and personal circumstances. By carefully considering these factors, seniors can develop a financial strategy that maintains growth and stability, ensuring their assets support their retirement goals and provide peace of mind in their later years.

How Age and Wealth Influence Investment Decisions in Later Life

As individuals approach their later years, the question of how to manage a substantial investment portfolio becomes increasingly pertinent. For those with a $3.5 million stock portfolio, the decision to rebalance to a 60/40 mix of stocks and bonds is a critical consideration. This decision is influenced by a variety of factors, including age, wealth, risk tolerance, and financial goals. Understanding how these elements interplay can guide investors in making informed choices that align with their long-term objectives.

Firstly, age is a significant factor in determining investment strategy. As individuals enter their 70s and beyond, the need for capital preservation often becomes more pronounced. The traditional 60/40 portfolio, which allocates 60% to stocks and 40% to bonds, is designed to balance growth potential with income generation and risk mitigation. This mix can provide a buffer against market volatility, which is particularly important for older investors who may not have the luxury of time to recover from significant market downturns. However, it is essential to recognize that age alone should not dictate investment decisions; rather, it should be considered alongside other personal circumstances.

Wealth is another crucial consideration. A $3.5 million portfolio offers a level of financial security that allows for greater flexibility in investment choices. For some, maintaining a higher allocation to stocks may be desirable to continue growing their wealth, especially if they have other sources of income or a robust safety net. Conversely, those who rely heavily on their portfolio for living expenses might prioritize stability and income, making the 60/40 mix more appealing. The key is to assess how much risk one is willing to take and how much income is needed to sustain their lifestyle.

Moreover, risk tolerance plays a pivotal role in shaping investment decisions. While some individuals are comfortable with the inherent volatility of a stock-heavy portfolio, others may find the potential for large fluctuations unsettling. A 60/40 mix can offer a compromise, providing exposure to the growth potential of equities while cushioning against market swings with the relative stability of bonds. It is important for investors to regularly reassess their risk tolerance, as it can evolve with changes in personal circumstances and market conditions.

In addition to these factors, financial goals must be considered. For some, leaving a legacy for heirs or charitable causes is a priority, which may influence the decision to maintain a more aggressive investment stance. For others, the focus may be on ensuring a comfortable retirement without the stress of market volatility. Understanding one’s financial objectives can help clarify whether a 60/40 portfolio aligns with their aspirations.

In conclusion, the decision to rebalance a $3.5 million stock portfolio to a 60/40 mix at age 70 and beyond is multifaceted. It requires careful consideration of age, wealth, risk tolerance, and financial goals. By evaluating these factors, investors can make informed decisions that reflect their unique circumstances and priorities. Ultimately, the goal is to create a portfolio that not only meets current needs but also provides peace of mind for the future. As with any financial decision, consulting with a financial advisor can provide valuable insights and help tailor a strategy that best suits individual needs.

Q&A

1. **What is a 60/40 portfolio mix?**

A 60/40 portfolio mix refers to an investment strategy where 60% of the portfolio is allocated to stocks and 40% to bonds, aiming to balance growth and risk.

2. **Why consider rebalancing to a 60/40 mix at 70+?**

As individuals age, they may prioritize capital preservation and income over growth, making a 60/40 mix potentially more suitable for reducing volatility and providing steady income.

3. **What are the benefits of a 60/40 portfolio for retirees?**

It offers a balance between growth potential from stocks and income stability from bonds, helping to manage risk and provide a more predictable income stream.

4. **What are the risks of maintaining a high stock allocation at 70+?**

A high stock allocation can lead to increased volatility and potential losses, which may be challenging to recover from during retirement when income is often fixed.

5. **How does inflation impact a 60/40 portfolio?**

Inflation can erode the purchasing power of fixed-income investments like bonds, but the stock portion can provide growth potential to help offset inflation.

6. **What factors should be considered before rebalancing?**

Consider your risk tolerance, income needs, life expectancy, and market conditions before deciding to rebalance your portfolio.

7. **Is a 60/40 mix suitable for everyone over 70?**

No, suitability depends on individual financial goals, risk tolerance, health, and other personal circumstances. It’s important to tailor the strategy to your specific needs.

Conclusion

Rebalancing a $3.5 million stock portfolio to a 60/40 mix of stocks and bonds at age 70+ can be a prudent decision, depending on individual circumstances. A 60/40 portfolio is traditionally considered a balanced approach, offering growth potential through equities while providing stability and income through bonds. For individuals over 70, this strategy can help reduce exposure to market volatility, preserve capital, and generate income, which is crucial during retirement years. However, the decision should also consider factors such as risk tolerance, life expectancy, income needs, and other financial resources. Consulting with a financial advisor to tailor the strategy to personal goals and circumstances is advisable.

{kind=link}